The outright plunge by global bureaucrats towards their utopian of zero carbon targets by 2030s will create endless suffering to the people over whom they govern – a glance at the blue areas above shows how overwhelmingly dominant the global economy and people’s livelihoods are powered today by carbon sourced energy.

To impose a planned economy style hard target over the citizenry and deprive them of essential energy (red arrow) will surely return civilisation back to the stone ages – in other words, the impossibility to come up with a substitute energy capacity in such a short span of time (represented by the vertical orange arrow) means the global population, if all following this mad course of action, will be deprived of 85% of their current energy needs…

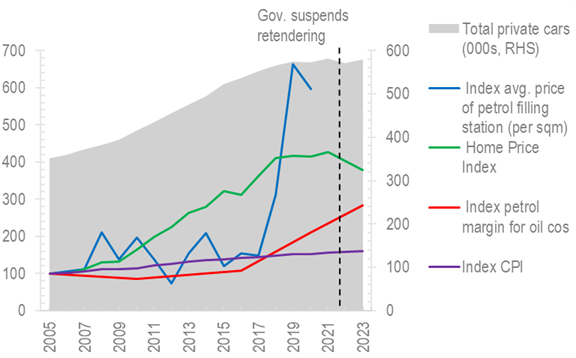

In view of the above, the HK govt should rapidly reverse its policy and start issuing new petrol station sites without delay – or consumers will continue to suffer.

A new model for petrol station licencing?

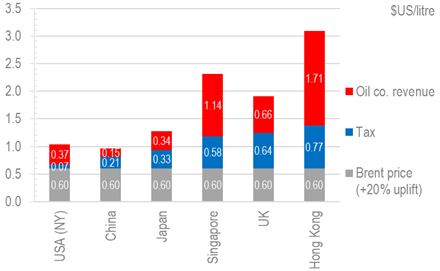

Back to the question of affordable fuel for the end user – the traditional way the HK government tenders out station sites has been on a land sale mentality – that is, with a view to selling the site areas to fetch the highest land revenue for the government and not with a purpose of creating a sustainable after market for the masses.

However, if we view petrol as an essential part of people’s daily needs, much like telephone and electricity then why should we not tender petrol stations on a different formula? Whereas the telephone exchanges and electric substations are pretty much given away for free, we submit that petrol stations should also be tendered out based on minimising future fuel costs.

The objective of controlling electricity costs is achieved by the Scheme of Control framework, which is based on return on capital invested. What we should do on petrol stations perhaps, is to have the oil companies bid for each station where the winner of the site is the one that promises the lowest price margins over the prevailing oil price at the time? Not only is this simple formula easy to monitor from an ongoing basis, it introduces a mechanism to drive down long term fuel costs and every economic sector of the society will benefit, rather than just the government’s one off land sale income. Which would you rather trust to keep the spoils from reduced oil company profits – the government or the people? The answer should be beyond dispute…

The author would like to thank Chan Hei Lui Kiandra from The University of Science and Technology majoring in Quantitative Finance for assisting in data collection and analysis of this article.