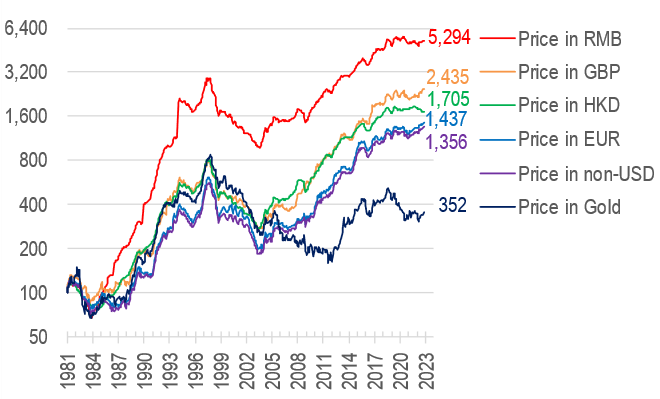

The observation that HK housing is in a downcycle has become consensus of late, after the CCL reaches a new low last week from the triple top dating as far back as 2019 (see green line in Chart 1). Cumulatively the index is now down 12% from the Aug 2021 high:

Chart 1: Home prices denominated in various currencies

But across the world, investors will always think about returns in their own currencies, and therefore, an ‘objective consensus’ of a true bear market in any asset price is only formed when the bulk of observers around the world see the same down trend that the base currency investors also sees.

So in order to find out whether the HK home prices are truly in a bear market by consensus (Chart 1 does not seem to suggest that is the case), let’s take a look at the index as denominated in a few main jurisdictions:

a) the collective non-USD community (as proxied by DXY); b) the EU community (as proxied by Euro); c) the Brits (as proxied by GBP); and d) gold bugs (as proxied by the price of gold).

HK still in bull market to world at large

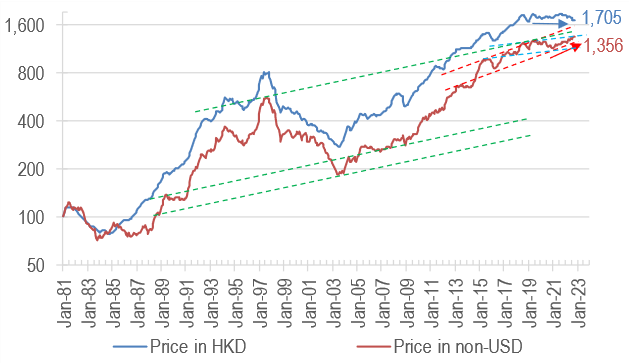

From the point of view of the developed world population (as the USD index is represented by six liquid currencies, see Chart 3), however, the drop in HKD (blue line in Chart 2) terms is not corroborated by the price as measured by DXY the USD index:

Chart 2: Home price in non-USD terms still trending up

In fact, the non-USD price index is still very much heading up, from the longer term view (green dotted lines) to medium term view (red dotted lines), to even the shorter term time horizon (blue dotted lines)! What this suggests is that for the average OECD investor, HK property is still a rising asset.

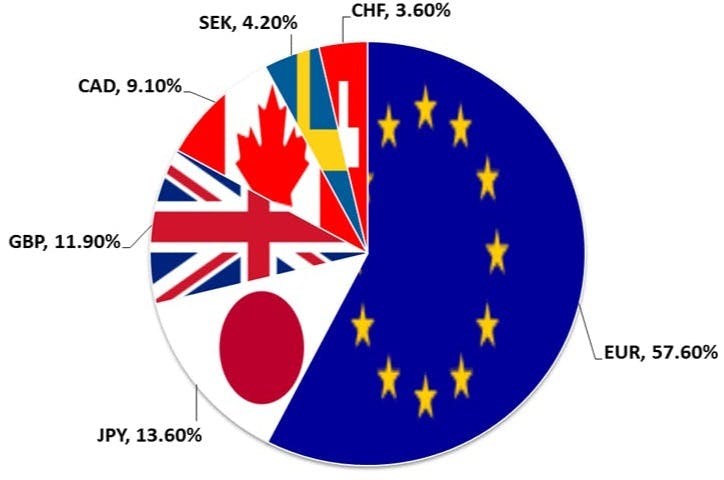

Chart 3: make up of the DXY – 6 currencies

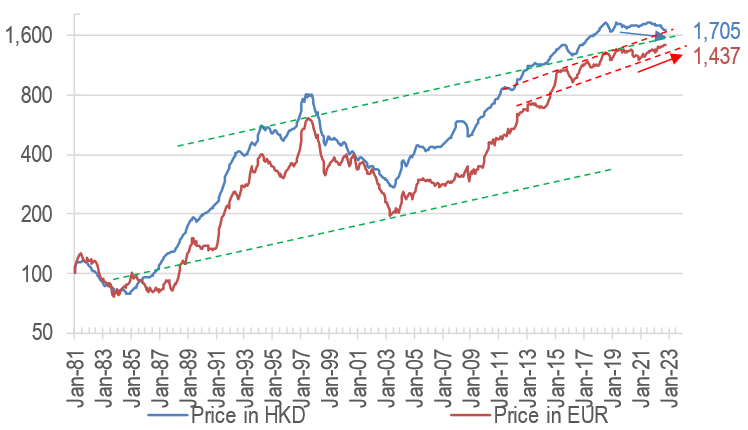

Home prices even more bullish for Europeans

For the average person based in Euro, the upward momentum seems even stronger compared to DXY, and HK prices, thanks to the collapse in Euros in the last few months, seem to be accelerating upwards within the red channel:

Chart 4: Euro investors may see HK prices accelerating upwards

Brits also feel the upturn?

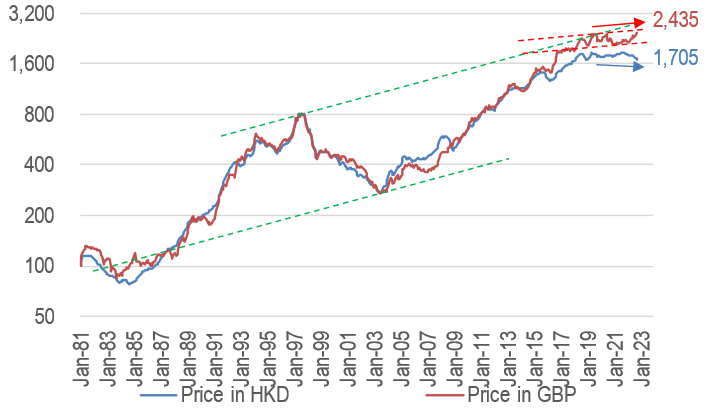

Similarly, with the recent precipitous drop in the value of the Pound, the HK home price index will appear to the average Blighty investor to be positively surging even, after HK first started pulling away from a very correlated pairing between the HKD and GBP denominated indices which pretty much shadowed each other since our data started in 1981:

Chart 5: HK prices look strong to the British Pound investor

The much weaker pound post Boris’s premiership (botched Brexit plus zealous lockdowns?) ensures that the weak pound has provided a strong platform for HK assets to appear to go from strength to strength.

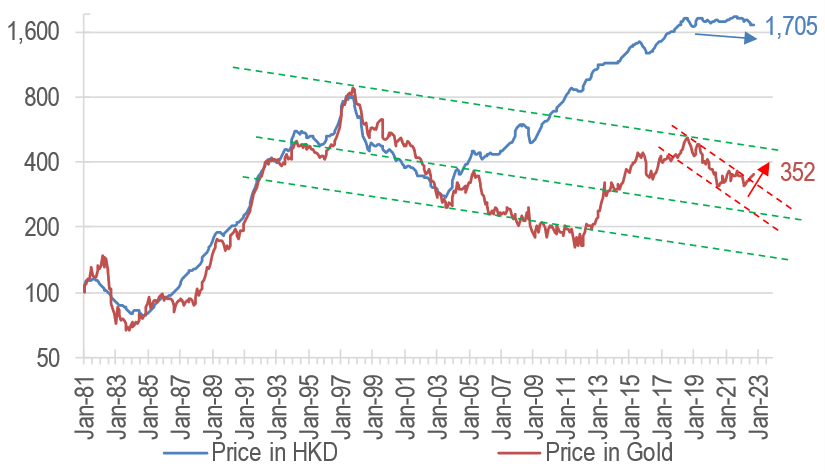

Gold the only currency beating HK property?

For those who believe in gold, there is good news – In Gold terms, the 1997 peak remains the unsurprised top for HK home prices, meaning that we may still be in a bear market when measured from the perspective of the precious metal:

Chart 6: Gold strong vs HK, but mini breakout underway?

Even though the price index has broken above a near term trading channel, as indicated by the red arrow in Chart 6, if war does flare up more next year, we think gold might reassert its dominance and the break up could reverse. Time will tell.

Strong currency imports deflation, which is not a bad thing now!

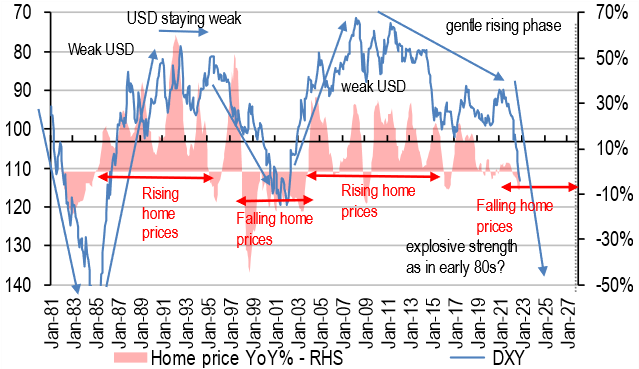

In normal disinflationary times such as most of the past 40+ years, being pegged to the USD is good for HK assets during times of weak USD, as Chart 7 illustrates – weakening or weak USD is generally accompanied by bouts of strong home price increases, and the reverse held true (mostly in the mid/late 90s):

Chart 7: weak USD good for home prices, and vice versa – will it be different this time?

However, could we be in a period similar to the early 70s or early 80s, when strong USD will suck liquidity away from HK and produce deflation? How does this contrast the current super high inflationary environment? Is the strong USD a blessing as it reduces the ‘cost of living’ crisis that would otherwise hit these shores?

A very interesting dynamic, not seen before in our brief monetary history for sure… The above study shows that, whilst we remain somewhat bearish on the outlook of the HK market, more needs to happen in the global currency markets before it is a true foregone conclusion…

The author would like to thank Lee Man Hin Carson from The University of Hong Kong majoring in Accounting and Finance for assisting in data collection, analysis, and drafting of this article.