In view of recent reports of HK fiscal deficits, the pundits are yet again out in force, staging the tired chorus (including the organisation never engaged in any profitable enterprise, the IMF) of how HK’s tax take is too volatile and we should reform to ‘broaden the tax base’ and so on and so forth, to the point that even the HKSAR govt has been hypnotised into starting its own initiative looking into this most unsuitable direction to take for an open economy which survives on being a ‘super connector’ (this is the HKSAR’s own term!) of people, goods, capital, and ideas:

Figure 1: resist the temptation Chief Executive Lee, stay narrow and stay competitive

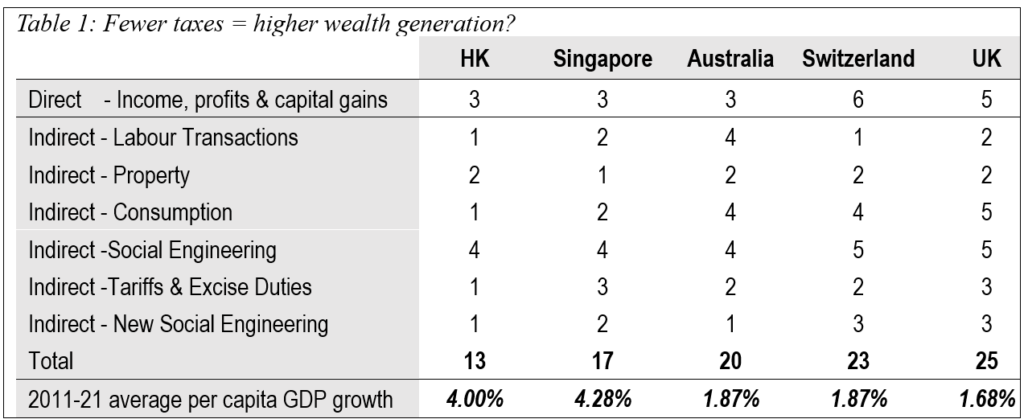

To illustrate the point more explicitly, we have compiled the total number of levies in the key subcategories of taxation for a number of jurisdictions (HK vs Singapore and Switzerland as small open regions, and Australia and UK as traditional OECD large economies). What is clear from the exercise is that the fewer taxes levied in an economy, the higher the economic growth, and vice versa:

We further collected all the government revenue information of the same jurisdictions and put them in the same general groupings but shown in proportion of total revenues.

It is worth quickly explaining what the tax groupings are:

- direct taxation on people’s economic activities – ie tax on income, profits & capital gains;

- indirect taxes, in the following activity groupings:

- taxes levied on labour market activities (eg payroll taxes, royalties);

- taxes on property transactions (mostly stamp duty and rates);

- taxes on consumption (ie GST, VAT, plus vehicle and insurance taxes);

- traditional social engineering levies (the so called sin taxes on gambling, alcohol, tobacco);

- new social engineering levies (all the woke and communistic charges that became so popular in recent years, such as climate change tax, carbon credits); and

- border related tariffs/duties (besides traditional tariffs we also include airport taxes – essentially a charge on foreign people crossing borders).

We argue below how careful design of tax regimes can serve as important factors in promoting the competitiveness and economic vibrancy of an economy, and how the proportions need to be adjusted as policy priorities that all governments should pay attention to.

Open free economies tax less on income

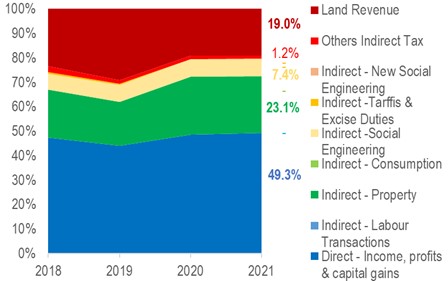

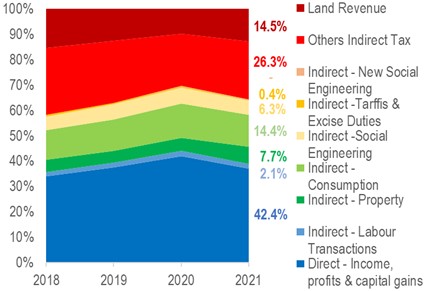

What jumps out from the charts below are that Hong Kong and Singapore rely on significant land sale revenues (dark red in Charts 1 and 2) as their fiscal income, which helps when both are amongst the most expensive property markets in the world!

Further, HK’s simple and low tax regime as an advantage is also clear – 4 of the tax categories had nil, or near zero incomes, making it low friction for commerce, and less cumbersome administration of the same taxes as would be the case in other countries. Singapore is less simple but still has one near-zero intake category (thankfully the ‘new social engineering’ group).

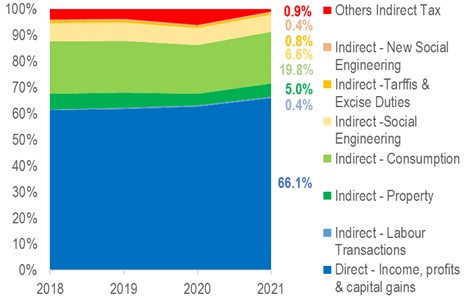

Finally, both city economies have much lower direct tax takes – with HK at 49% and Singapore an even lower 42% (dark blue area) – thus rewarding work and enterprise more than their bigger competitors:

Chart 1: HK govt income – low on direct taxation

Chart 2: Singapore GST helps reduce other tax burden

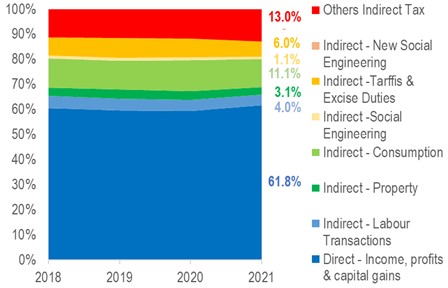

In the other extreme, UK’s takes more out of income (66% of tax revenue is from income/profit taxes) than all the jurisdictions in our study; of what is left in the tax payer’s pocket, the UK takes a larger slice through consumption taxes (19.8% of tax take vs Australia’s 11.1%, light green in Chart 4) than the other countries. Besides higher tax on income and consumption, the UK also has the most number of headings under which it taxes its people, making it even more unpalatable for the average wage earning tax payer:

Chart 3: Percentage of Tax Revenue Breakdown in Australia

Chart 4: Percentage of Tax Revenue Breakdown in UK

Isn’t it ironic therefore that the proponents of ‘broader tax base’ are heeding the preachings coming from largely high tax jurisdictions?

Can HK cancel income/profit tax and levy sales tax instead?

The USA did not have income tax until the 16th Amendment was passed in 1913, before that Article 1, Section 9, Clause 4 of the US constitution forbade direct taxation explicitly. The fact that this provision was inserted in Article 1 of the constitution is significant evidence that the founding fathers did not intend the state to infringe on the freedom of the people to generate and keep their own wealth.

HK’s situation is perhaps also conducive to a move away from income taxes – by virtual of its vast trade and re-export flows, immense tariff or sales tax intake could be achieved without burdening either its wage earning population, or profit making enterprises.

The other advantage of a move from income tax to sales tax is the more stable income stream compared to volatile sources such as land sales and even income/profits taxes.

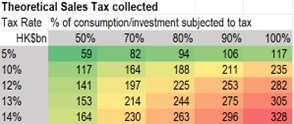

Theoretically speaking, private consumption expenditure, when taxed at a mere 10% tax rate on 80% of total consumption can already generate HK$188billion of revenue (Table 2):

Table 2: Theoretical sales tax collectable for various tax rate scenarios

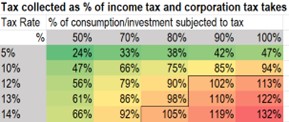

Table 3: Sales tax at 14% on 80% of consumption more than covers all income tax and corporation tax takes

In other words, Hong Kong can collect enough sales tax with a rate of 13.5% on 80% of private consumption expenditure to cover all the income and corporation taxes foregone if we were to make such a transition tomorrow.

Revisiting study: less income tax leak = more economic growth

In our earlier research looking at tax composition amongst US states, it was clear that more sales tax than income tax allows people keep more of their wealth, and is better for ecnomic growth, and similarly giving individuals equal or better treatment than company also engenders prosperity (the study can be seen here – English: web, blog, linkedin, facebook; Chinese: web, blog, linkedin, facebook).

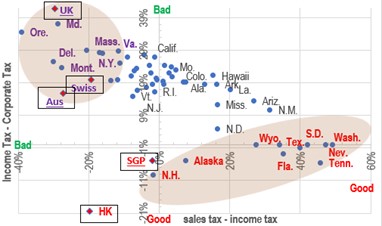

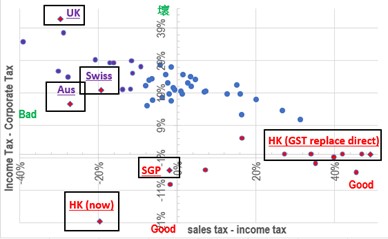

Adopting the same analysis in the prior study, we now add our five candidate tax regimes to the study, by plotting them on the same two measurements:

- sales tax less income tax (x axis) – higher value means consumption rather than savings are being taxed, thus encouraging investment for longer term;

- income tax less corporation tax (y axix) – a low reading indicates either there is a booming corporate sector or individuals get to keep more of their salaries.

Below chart shows that with current tax compositions, HK and Singapore (near the red states) are better positioned than Switzerland/Australia/UK which are situated in the more oppressive quadrant (amongst the purple states) of the original distribution:

Chart 5: lower income tax for HK/SGP suggests better economic prospects

Then if we replace all HK income/corporation taxes with sales taxes as outlined above, HK’s position improves massively – becoming the jurisdiction furthest right in the study universe (right hand red diamond, Chart 6) and leaving Singapore well and truly in the dust:

Chart 6: by replacing income/corporation tax with sales tax, HK beats all US states on tax attractiveness

The above scenario places Hong Kong very much near (if not at) the top of the (Sales Tax – Income Tax) axis amongst the 130+ countries in the world collecting sales taxes. By abolishing the income and corporation taxes, Hong Kong’s global competitiveness and attractiveness for almost all global companies and high income talents, not to mention vast amounts of tax refugees in developed countries where simply being rich is a sin, and having income anywhere outside the country’s borders is a reason to be taxed.

Given the significant benefit of not just economic attractiveness, but also a massive reduction in administrative burdens that the whole tax collection bureaucracy brings with the income/corporation tax regimes, improvements in citizen’s privacy standards (no need to declare what, how, and when you earn your incomes), Hong Kong can truly become a beacon of freedom and commerce. Chief Executive Lee and Financial Secretary Chan should ignore the cacophony of calls from vested interest groups calling for ‘boradening tax base’ including accountants, regulators, and academics, whose livelihood only improves if we have complex and oppressive tax systems, for it is they who get work / compensations when we go down that road. HK deserves better.

The author would like to thank Tia Yik Ethan from The University of Hong Kong majoring in Finance for assisting in data collection, analysis, and drafting of this article.

Below tax proposal by candidate Trump rhymes exactly with what we proposed for HK’s tax way forward in the article above – remove the disincentive to work and enrich, and tax instead spending (and profligacy)’:

_________________

https://www.nytimes.com/2024/10/24/us/politics/donald-trump-tax-policy.html

“It had all tariffs — it didn’t have an income tax,” Trump said. “Now we have income taxes, and we have people that are dying. They’re paying tax, and they don’t have the money to pay the tax.”

Overspending and bureaucratic enlargement is always against the interest of the hard working tax payers – instead of cutting expenditure, the govt again plots against the people:

_________________

https://finance.mingpao.com/fin/instantf/20250116/1736993667086

HK needs to spend within its means, not raising debts, because that will lead to higher taxes and people deserting the city, just like they are doing to CA

https://x.com/SanDiegoKnight/status/2048900058301739102