Given the importance of the subject matter and its ability to impact everyone’s financial arrangements in the coming years, we are putting the below internal client communication out in the public domain, hoping to contribute to clarify what actually happened in the liquidity crisis initially couched as a crypto crisis.

—————————

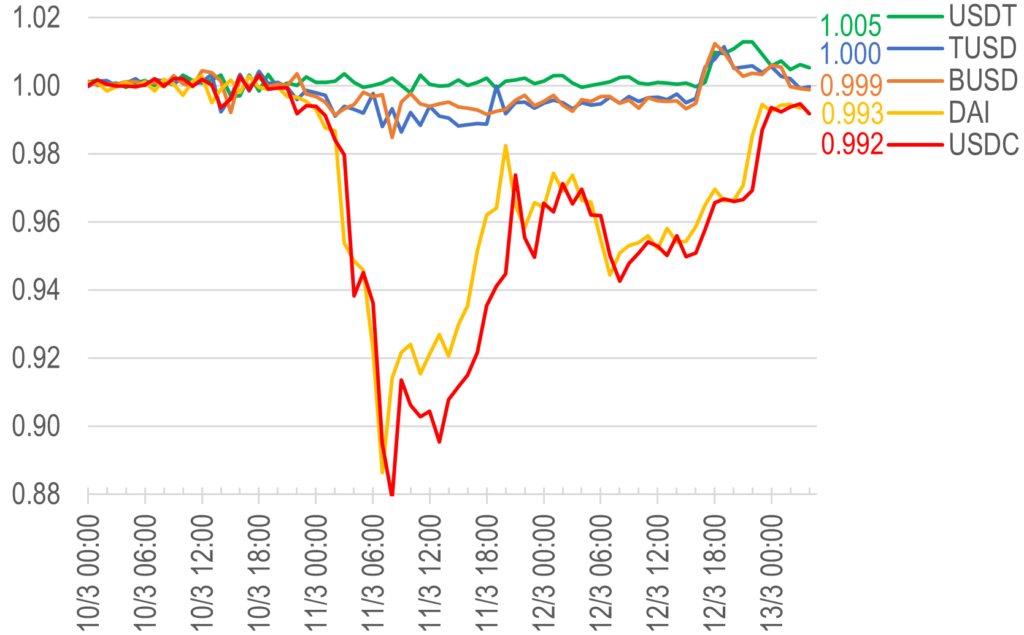

The depegging of the USDC stablecoin over the weekend was a big event, as it could have shake the confidence in what is deemed the safest of all the stablecoins. There was quite a roller coaster ride in both USDC and DAI (which holds some USDC as its reserve backing), which now seem to be all good again after govt guarantees were rushed out late Sunday:

Crypto banks – the Sudden Wipe Out Syndrome?

Whilst it is easy to characterise the incident as another ‘nail in the coffin’ of cryptos, a look under the hood reveals that this is a banking/liquidity problem – deposit taker (or SVB) going bust and not the stablecoin operator, who has barely jumped ship from another bankrupt bank (i.e. Silvergate Bank) some 10 days ago (see details here)!

What seems odd though is that these close banking allies of the crypto ecosystem seem to be going under eerily close together – Signature Bank also got taken over by the govt (article 1) citing liquidity issues also.

With these entities now killed off in short succession, some in crypto space might question could this be not random occurrences just when govts are starting to launch their own CBDCs (central bank digital currencies)? Without these on/off ramp channels, how could the crypto space continue to grow?

The 4 Hoursemen of debt apocalypse?

Irrespective of what possible coincidences/agenda against the crypto industry may be speculated, what we see in the bigger picture is that we are in the early phase of a bond default crisis that has been decades in the making:

a) ever lower record low interest rates has created bias for buying and holding ‘risk free’ govt bonds (sometimes mandatory, eg pension funds) that have now become toxic, especially long dated ones, thanks to the 4 massive negatives (you may call them the 4 horsemen of bond demise) that will keep bonds risky:

1) record govt debts are driving risk premium up and will keep worsening as rates increase;

2) geopolitical separation will drive deglobalisation for years to come (so no more cheap goods, which will get dearer for years to come),

3) lockdowns and net zero carbon agenda will drive higher energy costs for years to come, rippling into other costs throughout all supply chains; and

4) the war in Ukraine and likely WW3 will worsen both risk premium and supply chain disruptions

b) stuck in old theories, central banks keep hiking rates chasing inflation as it spirals out of control, creating banking/liquidity crises like the one we are seeing now – ie bank/pension balance sheets crash as bond prices collapse – resulting in solvency/liquidity concerns which lead to bank runs.

To understand how bond illiquidity and pervasive govt prescription on risk management has resulted in the mess we are now in, look at Bill Ackman’s short diagnosis (article 3) or Dan Lacalle’s longer missive (article 2), and finally how mobile banking + instant social media could create flash bank runs at the drop of a hat (article 4).

Seek protection in Anything But Bond/cash?

So we know this debt bust will be inevitable, how can we protect ourselves? There are several levels to position:

1) stay in the best quality and most liquid market, avoid the weaklings (eg most EU bonds/currencies, even JPY /JGBs which will suffer more in rate hike race) vs US – both cash and short dated bills;

2) park money in real assets (property/stocks/ precious metals/ even crypto) – when bond market, many times the size of equities trigger capital flights, the flood will likely be overwhelming, just buy in safe places (eg away from conflicts) or sectors that will not suffer from the cost of capital spike (eg tech);

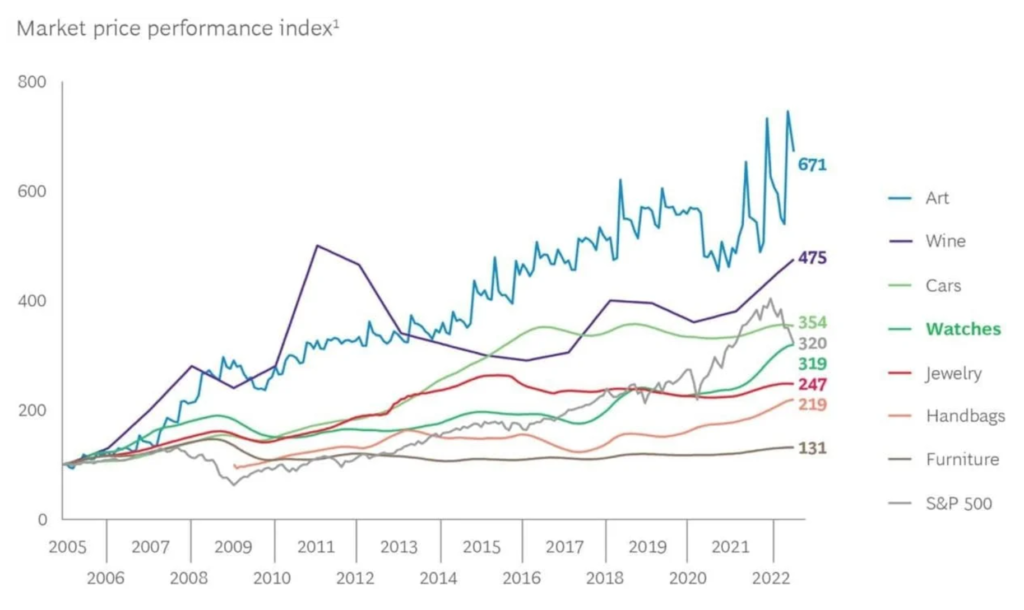

3) more esoteric but more mobile/ alternative / off-grid assets such as paintings, antiques, etc, here is one chart that illustrates how the trend is very much underway already:

Void in crypto on/off ramping – will be filled soon?

Perhaps the Nigerian disastrous CBDC launch is one example:

Nigerians’ Rejection of Their CBDC Is a Cautionary Tale for Other Countries

Digital-Currency Plan Falters as Nigerians Defiant on Crypto

Just like gold’s longevity in the age of fiat currencies, crypto will probably become the new digital version of gold in the CBDC dominated future…

MAR 12 20236:24 PM EDT

U.S. regulators on Sunday shut down New York-based Signature Bank , a big lender in the crypto industry, in a bid to prevent the spreading banking crisis.

“We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority,” Treasury, Federal Reserve, and FDIC said in a joint statement Sunday evening.

The banking regulators said depositors at Signature Bank will have full access to their deposits, a similar move to ensure depositors at the failed Silicon Valley Bank will get their money back.

…

Signature is one of the main banks to the cryptocurrency industry, the biggest one next to Silvergate, which announced its impending liquidation last week.

…To stem the damage and stave off a bigger crisis, the Fed and Treasury created an emergency program to backstop deposits at both Signature Bank and Silicon Valley Bank using the Fed’s emergency lending authority.

The FDIC’s deposit insurance fund will be used to cover depositors, many of whom were uninsured due to the $250,000 guarantee on deposits.

https://www.cnbc.com/2023/03/12/regulators-close-new-yorks-signature-bank-citing-systemic-risk.html

12 March, 2023 | Daniel Lacalle

<below are summary points only>

– The Silicon Valley Bank Collapse Is a Direct Consequence of Loose Monetary Policy

– The demise of the Silicon Valley Bank (SVB) is a classic bank run driven by a liquidity event, but the important lesson for everyone is that the enormity of the unrealized losses and financial hole in the bank’s accounts would have not existed if it were not for ultra-loose monetary policy

– the bank’s liquidity event could not have happened without the regulatory and monetary policy incentives to accumulate sovereign debt and mortgage-backed securities.

– The bank’s assets …More than 40% were long-dated Treasuries and mortgage-backed securities (MBS). The rest were seemingly world-conquering new tech and venture capital investments.

– Most of those “low risk” bonds and securities were held to maturity. They were following the mainstream rulebook: Low-risk assets to balance the risk in venture capital investments.

– The entire asset base of SVB was one single bet: Low rates and quantitative easing for longer. …these were the lowest risk assets according to all regulations and, according to the Fed and all mainstream economists, inflation was purely “transitory”, a base-effect anecdote. What could go wrong?

– Inflation was not transitory and easy money was not endless.

– Rate hikes happened. And they caught the bank suffering massive losses everywhere. Goodbye bonds and MBS price. Goodbye tech “new paradigm” valuations. And hello panic. A good old bank run, despite the strong recovery of the SVB shares in January. Mark-to-market unrealized losses of $15 billion were almost 100% of the market capitalization of the bank. Wipe out.

– SVB showed how quickly the capital of a bank can dissolve in front of our eyes.

– SVB did exactly what those that blamed the 2008 crisis on “de-regulation” recommended. SVB was a boring and conservative bank that invested the rising deposits in sovereign bonds and mortgage-backed securities and believed that inflation was transitory as everyone except us, the crazy minority, repeated.

– SVB did nothing but follow regulation and monetary policy incentives and Keynesian economists’ recommendations point by point. SVB was the epitome of mainstream economic thinking. And mainstream killed the tech star.

– Many will now blame greed, capitalism and lack of regulation but guess what? More regulation would have done nothing because regulation and policy incentivize adding these “low risk” assets. Furthermore, regulation and monetary policy are directly responsible for the tech bubble.

– SVB invested in the entire bubble of everything: Sovereign bonds, MBS and tech. Did they do it because they were stupid or reckless? No. They did it because they perceived that there was exceptionally low to no risk in those assets. No bank accumulates risk in an asset they believe has considerable risk. The only way in which a bank accumulates risk is if they perceive that there is none. Why do they perceive it? Because the government, regulators, central bank, and the experts tell them so. Who will be next?

– Many will blame everything except the perverse incentives and bubbles created by monetary policy and regulation and will demand rate cuts and quantitative easing to solve the problem. It will only worsen. You do not solve the consequences of a bubble with more bubbles.

https://www.dlacalle.com/en/silicon-valley-bank-followed-exactly-what-regulation-recommended/

…Absent @jpmorgan @citi or @BankofAmerica acquiring SVB before the open on Monday, a prospect I believe to be unlikely, or the gov’t guaranteeing all of SVB’s deposits, the giant sucking sound you will hear will be the withdrawal of substantially all uninsured deposits from all but the ‘systemically important banks’ (SIBs). These funds will be transferred to the SIBs, US Treasury (UST) money market funds and short-term UST. There is already pressure to transfer cash to short-term UST and UST money market accounts due to the substantially higher yields available on risk-free UST vs. bank deposits. These withdrawals will drain liquidity from community, regional and other banks and begin the destruction of these important institutions. The increased demand for short-term UST will drive short rates lower complicating the @federalreserve’s efforts to raise rates to slow the economy. Already thousands of the fastest growing, most innovative venture-backed companies in the U.S. will begin to fail to make payroll next week. Had the gov’t stepped in on Friday to guarantee SVB’s deposits (in exchange for penny warrants which would have wiped out the substantial majority of its equity value) this could have been avoided and SVB’s 40-year franchise value could have been preserved and transferred to a new owner in exchange for an equity injection.

…The gov’t’s approach has guaranteed that more risk will be concentrated in the SIBs at the expense of other banks, which itself creates more systemic risk. For those who make the case that depositors be damned as it would create moral hazard to save them, consider the feasibility of a world where each depositor must do their own credit assessment of the bank they choose to bank with. I am a pretty sophisticated financial analyst and I find most banks to be a black box despite the 1,000s of pages of @SECGov filings available on each bank. SVB’s senior management made a basic mistake. They invested short-term deposits in longer-term, fixed-rate assets. Thereafter short-term rates went up and a bank run ensued. Senior management screwed up and they should lose their jobs. …

10:38 pm · 11 Mar 2023

…

The important question is why so many demanded their money back at once. And I’m not referring to the last two days. I’m asking about the days/weeks leading up to this last two days forcing SVB to sell securities and realize a $1.8B loss, necessitating a capital raise. Why were depositors withdrawing in big enough amounts before Thursday/Friday?

First, welcome to the world of mobile banking. Gone are the frictions of standing in line with tellers instructed to count money slowly. (Media images of lines Friday were largely gawkers)

How did $42 billion get withdrawn Friday alone without thousands in line? Answer, your phone! This is not the Bailey Savings and Loan anymore.

This should scare the hell of bankers and regulators worldwide. The entire $17 trillion deposit base is now on a hair trigger expecting instant liquidity.

Add in social media and millions get a message, like Peter Thiel telling Founders companies to pull out, or Senator Warren gloating that SI went under, and pick up their phone open a Chase account and Venmo-ed their life savings into it in 10 minutes. Instant liquidity (not solvency) crisis with everyone still in bed.

Banking will never be the same.

…

What needs to be done? Two things.

The FDIC needs to raise the deposit insurance ceiling to unlimited as they did this in 2008. Besides $250k is a made up number anyway. So make up a bigger number.

Banks need to get their deposit base to stop figuring out how to buy a 4.5% money market fund. They need to raise the interest rates they pay 3.00% – 3.50%, from 0.50%, immediately. Yes, this will kill bank profitability so expect Bank Execs to balk at doing this.

This way the public gets the message that you money is safe, no matter the bank, or the amount, and the rate paid on your money is at least competitive with other alternatives. So, do nothing.

Otherwise, if we are all waiting for the Fed to START a meeting at 11:30 Monday, hundreds of billions of deposits will have moved by phone and it will be far worse.

https://twitter.com/biancoresearch/status/1634885127179325440